Are you overdiversified?

Is there such a thing as being too diversified? Isn’t more diversification always better?

Not always. It depends on your goals, your risk profile, and your expertise. You could be leaving profits on the table.

Let’s be clear. Diversification is a critical aspect of any investment portfolio. Reducing concentration risk is of utmost importance. This is why index funds, ETFs, and other super-broad, diversified funds have become so popular. However, these investments are not the perfect solution for reducing all risks nor for reaching your full profit potential.

WHY DIVERSIFY?

Concentration Risk

The old adage of not putting all your eggs in one basket is obviously a key step when trying to reduce your portfolio’s concentration risk.

A 2018 study indicates that, in the long term, very few stocks persistently provide any substantial value to their investors. In fact, according to author Hendrik Bessembinder, only around 4% of stocks account for “the net gain for the entire U.S. stock market since 1926, as other stocks collectively matched Treasury bills.”[1]

This means that very few of the stocks you invest in will ultimately beat T-Bill returns in the end. Ouch. That is a painful truth. But just because a stock might underperform over a 50-year period doesn’t mean it won’t provide massive returns during a five-year growth window. The game isn’t about holding forever; it’s about capturing value during the ascent.

But ‘timing the market’ is notoriously difficult (impossible, really). You can’t be sure which stocks are going to be the winners and which are going to be the losers in the future. Even the investment gurus on TV don’t really know. And so the industry’s standard solution is to stop guessing and simply buy everything.

This inability to time the market is also why a high percentage of actively managed US large-cap investment funds (89.5%+ over 15 years) cannot even beat a no-cost, highly diversified index fund.[2] It’s no wonder, then, that people have gravitated toward investing in auto-pilot, low- or no-fee funds/ETFs that diversify to the teeth and require little to no management. Why pay for extra management services that will likely only reduce your end profit?

THE DOWNSIDE OF OVERDIVERSIFICATION

Risk = Potential Profit?

Is it possible to hold so many positions that your best options are diluted by your mediocre or even worst options? Absolutely.

Here’s the thing: no one ever beat the market by being the market. The most successful investors you know were likely not avoiding risk like a dirty four-letter word, but weighing it carefully, evaluating it, and leveraging it strategically to achieve a greater return.

One common example: most successful small business owners who started from scratch generally succeeded only after taking on a decent amount (if not an astronomical amount) of concentration risk by investing in their own business. It is not uncommon to find a business owner who mortgaged their own house to make ends meet, especially during the first few critical years. This is an extremely high level of concentration risk.

Clearly, this higher level of risk exposure is not a great fit for everyone, but it illustrates how calculated and leveraged risk can potentially lead to greater financial rewards. This is true in the stock market as well.

Undiscerning Diversification

It’s true that no one knows for sure which stocks are going to be winners and which will be losers. However, intelligent investors can make more educated decisions by looking carefully at a stock’s fundamental characteristics.

Why bother? Because if you only invest in a very broad ETF (like VTI or SPY) it means you are accepting the risk of investing in the very best stocks available and the very worst—even the companies that you really should have known better. This is like buying two gallons of milk, one with the very best due date and one with the worst, because you are pretty sure some good milk will be found between the two.

Look at any one of the most successful stocks currently on the market. Did it make an impressive profit for the last five years in a row? That is one indication of a company’s good health, but it is no guarantee. Let’s look further. Lower debt? High revenue growth? High dividend? Lots of cash flow? Great return on capital? Strong moat? Great leadership? The more positive indicators we can pile up, the more likely it is that this stock will perform better in the coming year compared to a different stock with equally negative indicators. It’s still no guarantee, of course, but why would we give our attention to stocks with a historically negative performance and no indication of improvement?

This is where the popular philosophy of “more stock market diversification is always better” breaks down. All other factors being the same, it is far better, in my opinion, to invest your money in a diversified portfolio filled with stocks having strong positive indicators while rejecting stocks with strong negative indicators. On the other hand, you don’t want to make the mistake of cutting out emerging stocks with great breakout potential, so you do want to be careful in your pruning.

Warren Buffett famously said, “We think diversification . . . as practiced generally, makes very little sense for anyone that knows what they’re doing…it is a protection against ignorance.”[3]

Systematic Market Risk

There’s another critical issue with focusing the majority of your investment funds in a passive index fund or ETF—your investment becomes exposed to a different kind of risk: systematic market risk. When the market itself crashes as a whole, as it did catastrophically in 2008, are you willing to simply crash with it? This is NOT a great strategy.

When the next crash comes, and it will, many investment advisors will mollify their clients by saying, “Don’t worry—the stock market always bounces back.” This is terrible advice. Many passive investors in 2008 lost more than 55% of their hard-earned retirement funds and were still trying to “bounce back” more than five years later![4][5] That’s not an investment strategy. That’s five years of lost profits! If you don’t have any protection against future downturns, you are planning to fail.

Market Cap Concentration Risk

Broad index/ETF funds are often riskier than people realize, especially in relation to the largest mega-cap stocks listed. As the largest companies grow larger and larger, they represent a larger percentage of your passive index fund allocation. Passive funds force you to buy more of a stock simply because it has become expensive (often overvalued), and less of a stock because it has become cheap (often undervalued). If one of the “Magnificent Seven” stocks has a major crash, for example, it can have a strong negative impact on your bottom line, even though you have diversified across the entire stock market in a passive ETF fund.

Inflexible Opportunities

Another serious shortcoming of passive index/ETF funds is that they are inflexible. Intelligent investors can often pivot when they recognize opportunities, taking advantage of the upside and increasing their profits. Broad, passive funds never take advantage of these opportunities.

THE SOLUTION

So if passive funds aren’t the answer, what is?

As mentioned above, risk can often represent an opportunity for greater profits, but all risks are NOT created equal. The key is to find the best possible risk-to-benefit scenario to match your risk tolerance level and investment expertise.

Again, diversification in general is a critical part of any healthy investment strategy—but we can go about it in a more intelligent way. Even if your risk tolerance is low, here are a few suggestions for maximizing your profits and avoiding the hidden risks of putting all your investment funds into broad index/ETF funds:

- Stop seeing broad index funds and ETFs as completely “safe.” They are particularly vulnerable to market-wide downturns, which can be devastating.

- Over time, develop the expertise to research company fundamentals. Consider weeding out the most likely losers. Continue to diversify broadly. Consider focusing a portion of your funds on stronger, currently trending stocks with exceptional fundamentals and apply downside protection (see below).

- Never become permanently committed to any specific stock, even if it happens to be the company you work for. Continue to monitor fundamentals and exit your positions when they become weak. Keep any stock position for at least one year, if possible, to avoid short-term capital gains tax.

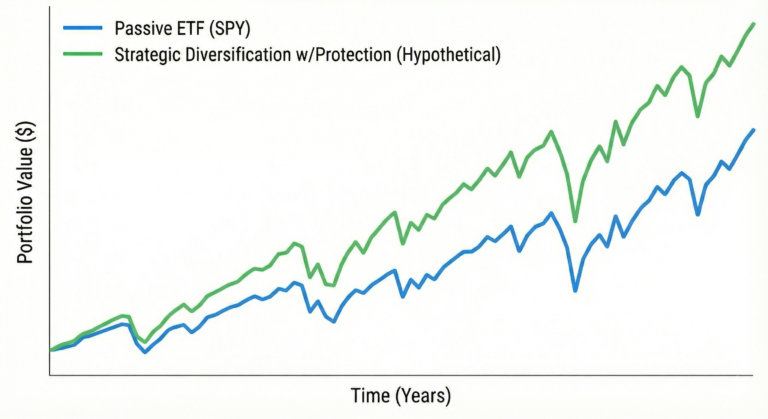

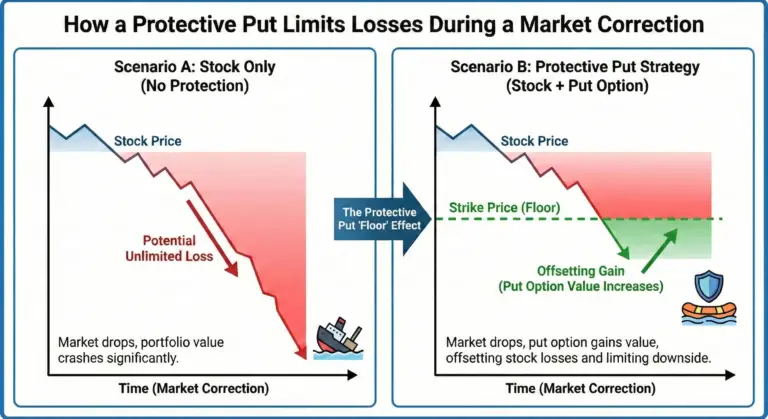

- Use protective puts and collars to protect your investments, especially in times of greater volatility. This is the secret sauce ingredient that many investors miss. Again, despite your amazing research skills, no one knows for sure which stocks will be the winners and losers. Anyone who says otherwise is selling you something or is simply deluded. This means that you must have a contingency plan in place. By paying more up front, you can effectively create an insurance-like protection against future downturns in key stocks in which you have a higher concentration. It is also possible to buy protective puts to protect your portfolio against market-wide corrections.

- When a stock price drops, buy even more stock at the lower price (assuming you still think the stock is fundamentally strong). This might seem counterintuitive, but this is one of the hallmarks of any good investor: always see downturns as a potential opportunity.

- Avoid fund managers who claim to know the future. They don’t. And anyone who is simply trying to time the market should be strictly avoided.

- Choose an investment advisor carefully. If you don’t want to actively trade stocks on your own but you still want to try to beat passive ETF returns, it is possible to find high quality investment firms who can effectively invest on your behalf (shameless plug for Hurley Investments here). Make sure the firm actively protects your funds against downturns. Look for a strong track record. The increased profits from the fund should not only pay for its own management, but it should also achieve sizable profits beyond. For example, Hurley Investments has been able to (historically) double portfolios every 4.5 to 5.5 years on average (note: this is on average—smaller returns or even losses for any specific year are not unusual). No firm can likely withstand a major market crash completely, but they should be able to seriously reduce your losses and your time to recovery in a time of crisis, while simultaneously taking advantage of lower stock prices at the dip. The best firms know how to use dollar cost averaging to turn a downturn into even higher profits in the long run.

Sources

Bessembinder, H. (2018). Do Stocks Outperform Treasury Bills? W. P. Carey School of Business, Arizona State University. View Study

S&P Dow Jones Indices. (2024). SPIVA® U.S. Scorecard. S&P Global. View Scorecard

Buffett, W. (1996). 1996 Annual Meeting: Afternoon Session [Video]. CNBC Warren Buffett Archive. View Archive

Rich, R. (2013). The Great Recession of 2007-09. Federal Reserve History. View History

Investopedia Staff. (2024). The Great Recession: What It Was and What Caused It. Investopedia. View Article